Most homeowners think the hard part of a hail claim is getting it approved. It isn’t. Approval is just the beginning. The real outcome is decided inside the estimate line by line, detail by detail. That’s where hail damage claim supplements come in, and where thousands of dollars are either recovered… or quietly lost. I’ve seen it happen over and over. A claim gets approved. The homeowner feels relief. The estimate looks clean and official. Then the contractor shows up, reviews the scope, and pauses. Something’s missing. Actually, a lot is missing.

Essential components aren’t listed. Measurements feel off. Code requirements? Not even mentioned. Now the homeowner is stuck in a frustrating position. Move forward and pay the difference? Or stop everything and push back? That gap between what’s written and what’s real is where claims are won or lost. And understanding hail damage claim supplements is what allows you to close it.

What Is a Hail Damage Claim Supplement?

Let’s get clear. A hail damage claim supplement is a formal revision to the original insurance estimate. It adds items that were missed, under-scoped, or incorrectly priced. This isn’t a loophole. It’s a correction.

Here’s how the process usually looks:

- Initial Scope: The insurance adjuster’s first estimate

- Discovery Phase: Additional damage or missing items are identified

- Supplement Submission: A revised estimate is created and submitted

- Revised Approval: The carrier reviews and issues additional payment

The key takeaway? The initial estimate is rarely the final version.

Why Insurance Carriers Miss So Much in Their Scope

It’s easy to assume mistakes shouldn’t happen. But the system itself creates gaps.

1. Time Pressure

Adjusters often inspect multiple properties per day. That pace doesn’t allow for deep, methodical analysis. Quick inspections lead to incomplete scopes.

2. Storm Volume

After hail events, claim volume spikes. In areas like Tyler, adjusters may be handling dozens of inspections in a short timeframe. Speed becomes the priority. Accuracy takes a hit.

3. Conservative Estimating Practices

Insurance estimates are built cautiously.

That means:

- Lower material quantities

- Fewer accessory items

- Minimal allowances for complexity

If something isn’t clearly documented, it’s usually excluded.

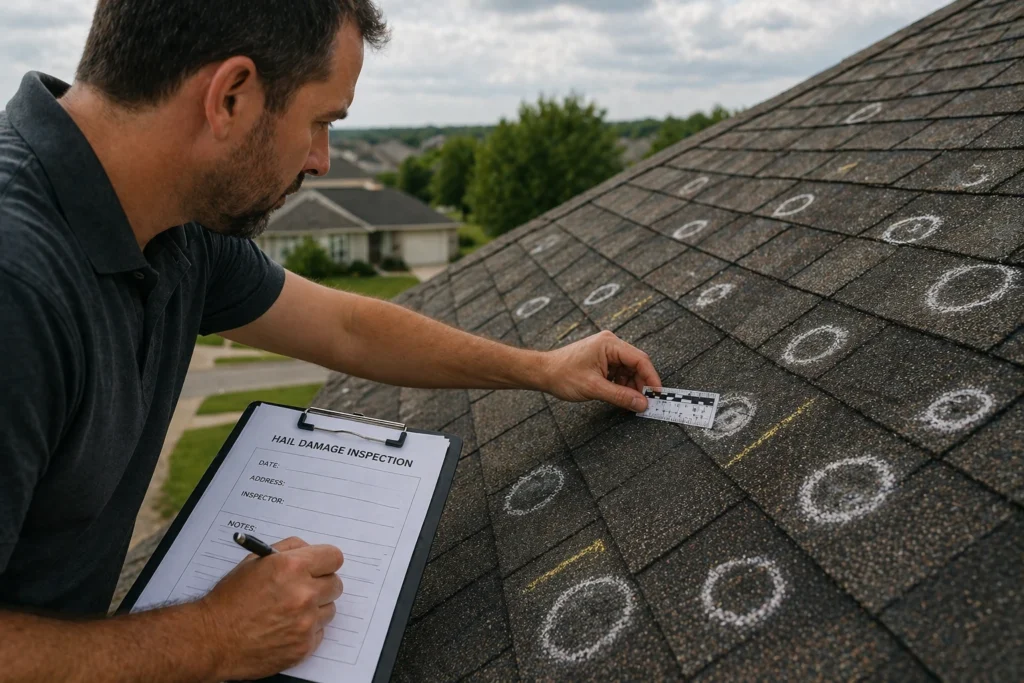

4. Documentation Gaps

No photo. No measurement. No note. Then it doesn’t exist in the estimate. This is one of the biggest reasons hail damage claim supplements are necessary.

The Most Common Items Missing From Hail Damage Scopes

This is where real money is lost.

Roofing System Components

A complete roofing system includes more than shingles.

Frequently missed items:

- Starter strips

- Ridge caps

- Drip edge

- Flashing

- Ventilation components

Each of these has a cost. Each one matters.

Code Upgrade Requirements

Building codes are not optional.

In Tyler and similar markets, code-related items may include:

- Ice and water shield

- Enhanced ventilation

- Decking standards

- Fastener requirements

If your policy includes ordinance or law coverage, these should be accounted for.

Exterior Damage

Hail impacts multiple surfaces.

Often overlooked:

- Gutters and downspouts

- Window screens

- Siding panels

- Paint finishes

Initial scopes frequently focus only on roofing, leaving these out.

Interior Damage

Interior damage often appears later. But it’s still part of the claim.

Missed items include:

- Ceiling stains

- Insulation damage

- Drywall repairs

- Paint blending

Why These Missing Items Matter Financially

Let’s quantify it.

| Scenario | Initial Estimate | After Supplement |

| Roof only | $9,800 | $15,200 |

| Roof + exterior | $12,500 | $20,300 |

| Full claim | $11,400 | $18,900 |

That gap is not inflated. It’s uncovered. Every missing line item adds up.

Understanding Xactimate: The Industry Standard

Xactimate is the estimating software used by most carriers.

It standardizes:

- Material costs

- Labor rates

- Equipment pricing

It also adjusts for location, meaning pricing reflects markets like Tyler. But here’s the truth. The software is only as accurate as the person using it.

How Xactimate Reveals What Carriers Miss

When used correctly, Xactimate exposes gaps.

Line-by-Line Detail

Each item is listed individually. No bundling. No vague totals.

Measurement Precision

Roof geometry affects everything. Incorrect measurements lead to underfunded claims.

Local Pricing Accuracy

Costs reflect real market conditions. Not guesses.

Code Integration

Required upgrades can be included if properly documented.

The Hail Damage Supplement Process (Step-by-Step)

Step 1: Re-Inspection

A detailed, methodical review.

Step 2: Documentation

Photos, measurements, notes.

Step 3: Estimate Creation

Built from scratch in Xactimate.

Step 4: Submission

Sent with full justification.

Step 5: Negotiation

Carrier review and response.

Step 6: Approval

Additional funds released.

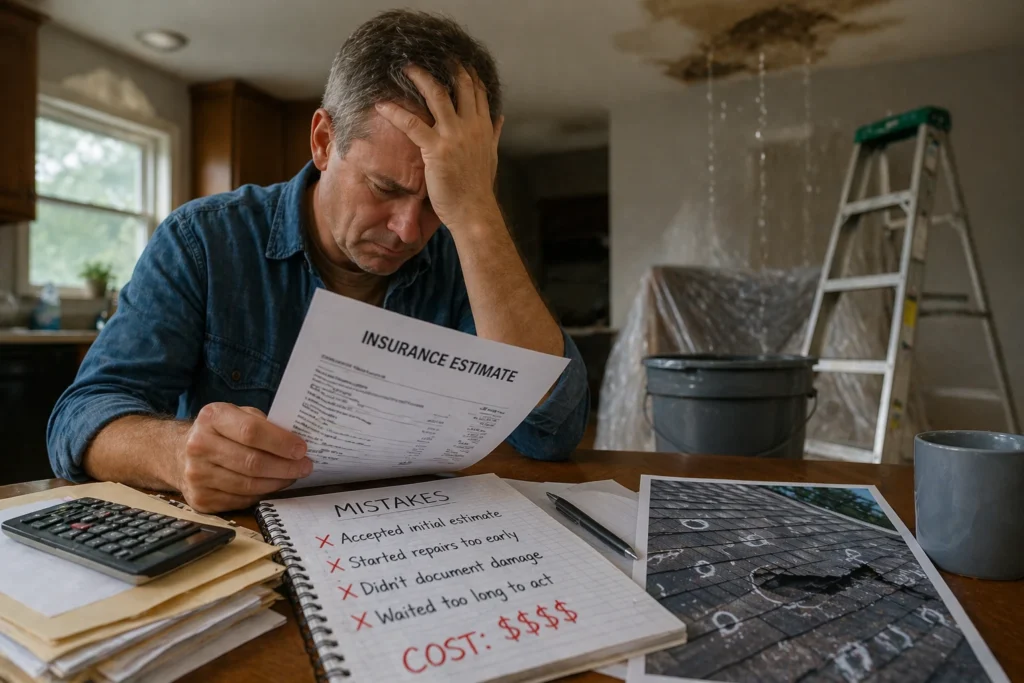

Common Mistakes Homeowners Make With Supplements

Avoid these:

- Accepting the initial estimate without review

- Starting repairs too early

- Failing to document damage

- Waiting too long to act

These mistakes cost money.

Contractor vs Public Adjuster: Who Handles Supplements Better?

| Role | Focus | Limitation |

| Contractor | Repairs | Limited negotiation |

| Public Adjuster | Claim value | Not performing repairs |

| Insurance Adjuster | Carrier interest | Cost control |

Public adjusters specialize in maximizing claim accuracy.

Real-World Example: Before and After a Supplement

Initial estimate: $10,900

Scope: Basic roofing

After supplement:

- Ridge caps added

- Drip edge included

- Ventilation upgraded

- Gutters replaced

- Interior repairs documented

Final total: $19,200

That’s the impact of hail damage claim supplements.

Red Flags in an Insurance Scope You Should Never Ignore

Watch for:

- Missing standard components

- Vague descriptions

- Low quantities

- No code references

These indicate an incomplete estimate.

How Homeowners in Tyler Can Protect Their Claim

If you’re filing in Tyler, attention to detail matters.

Protect your claim by:

- Documenting early

- Reviewing estimates carefully

- Asking questions

- Avoiding rushed decisions

When to Request a Hail Damage Claim Supplement

Act when:

- New damage appears

- The estimate feels incomplete

- Contractors identify missing items

- Interior issues develop

Timing is critical.

Advanced Supplement Strategies Using Xactimate

This is where expertise matters most.

Build From Scratch

Avoid inheriting errors.

Use Correct Line Items

Combine labor and materials properly.

Justify Code Items

Support with documentation.

Anticipate Pushback

Prepare strong submissions.

Deep Dive: What Carriers Commonly Push Back On

Let’s go deeper.

Carriers often question:

- High material quantities

- Labor-intensive items

- Code upgrades

- “Non-visible” damage

Why?

Because these increase claim cost. Your job or your adjuster’s job is to prove necessity.

That means:

- Clear photos

- Accurate measurements

- Strong explanations

A More Detailed Case Study: From Undervalued to Accurate

Let’s expand the earlier example.

Initial Estimate Breakdown:

- Roofing materials: $7,500

- Labor: $2,400

- Miscellaneous: $1,000

- Total: $10,900

What Was Missing:

- Starter strip replacement

- Ridge cap upgrades

- Drip edge installation

- Ventilation corrections

- Gutter replacement

- Interior ceiling repairs

Supplement Breakdown:

- Additional roofing components: +$3,200

- Exterior repairs: +$2,800

- Interior repairs: +$2,300

- Code upgrades: +$2,000

Final Total: $21,200

That’s nearly double the original estimate. Same damage. Fully scoped.

The Negotiation Playbook: How Supplements Get Approved

Let’s talk strategy.

1. Be Precise

General estimates get questioned. Detailed ones get approved.

2. Stay Consistent

Numbers, photos, and notes must align.

3. Communicate Clearly

Confusion slows approval.

4. Follow Up

Don’t submit and wait. Stay engaged.

The Psychology Behind Insurance Adjustments

Adjusters aren’t just reviewing numbers.

They’re evaluating:

- Credibility

- Consistency

- Documentation strength

Weak submissions invite resistance.

Strong ones move forward.

The Long-Term Cost of Ignoring Supplements

This isn’t just about today’s payout.

Incomplete claims lead to:

- Lower-quality repairs

- Future damage issues

- Reduced property value

You either fix it now or pay for it later.

Bringing It All Together

Let’s simplify everything.

Hail damage claim supplements are the bridge between:

- A partial estimate and a complete one

- Underpayment and full coverage

- Frustration and resolution

They are not optional.

They are essential.

Final Thought

If your estimate feels incomplete, it probably is. Trust your instincts. Ask better questions. Get a second opinion. Push for clarity. Because in this process, small details create big financial outcomes. And when handled correctly, hail damage claim supplements turn incomplete estimates into accurate ones—exactly the way they should be.

FAQs

Hail damage claim supplements are revisions to an insurance estimate that include missing or underpaid items after the initial scope is reviewed.

Initial inspections are usually fast and limited, which can lead to overlooked components, measurements, and code requirements.

You should request one as soon as you or your contractor notice missing items or additional damage not included in the original estimate.

They can extend the timeline slightly, but they often result in a more accurate payout, which makes the process worthwhile.

Yes, contractors can help identify missing items, but they may not handle negotiation as effectively as a public adjuster.

Xactimate is the software insurers use to create estimates, and accurate use of it ensures all materials, labor, and costs are properly included.

Not always approval depends on proper documentation, justification, and alignment with your policy coverage.

They can be included if your policy covers ordinance or law and the upgrades are properly documented and required.

You may end up paying out of pocket for missing items or settling for incomplete or lower-quality repairs.

Most supplements are reviewed within a few days to a few weeks, depending on the complexity and responsiveness of the carrier.