A denied claim hits hard. It’s frustrating, expensive, and honestly confusing. If you’re searching for what to do if your hail claim was denied in Texas, you’re already ahead of most homeowners. Why? Because you’re not accepting the first “no.” And that matters.

I’ve seen it over and over again especially with homeowners in Tyler a claim gets denied, the homeowner assumes that’s final, and thousands of dollars in legitimate damage go unpaid. But here’s the truth: a denial is often just the first round. Not the final decision. Handled correctly, many denied claims get reversed. Not by luck. By strategy. Let’s walk through exactly how to fight back and do it the right way.

Why Hail Claims Get Denied in Texas

Before you fix a denial, you need to understand it. Most denials follow predictable patterns.

Common Reasons for Denial

Insurance companies typically rely on a handful of explanations:

- Insufficient documentation

If your original claim lacked clear, detailed evidence, it weakens immediately. - Pre-existing damage claims

Insurers may argue the damage existed before the hailstorm. - Wear and tear vs. hail damage

This is one of the most common denial reasons and one of the most disputed. - Late filing

Waiting too long can give insurers leverage. - Policy exclusions

Some materials or types of damage may not be fully covered.

At first glance, these reasons can seem valid. But often, they’re incomplete or based on limited inspections.

Insurance Company Tactics You Should Recognize

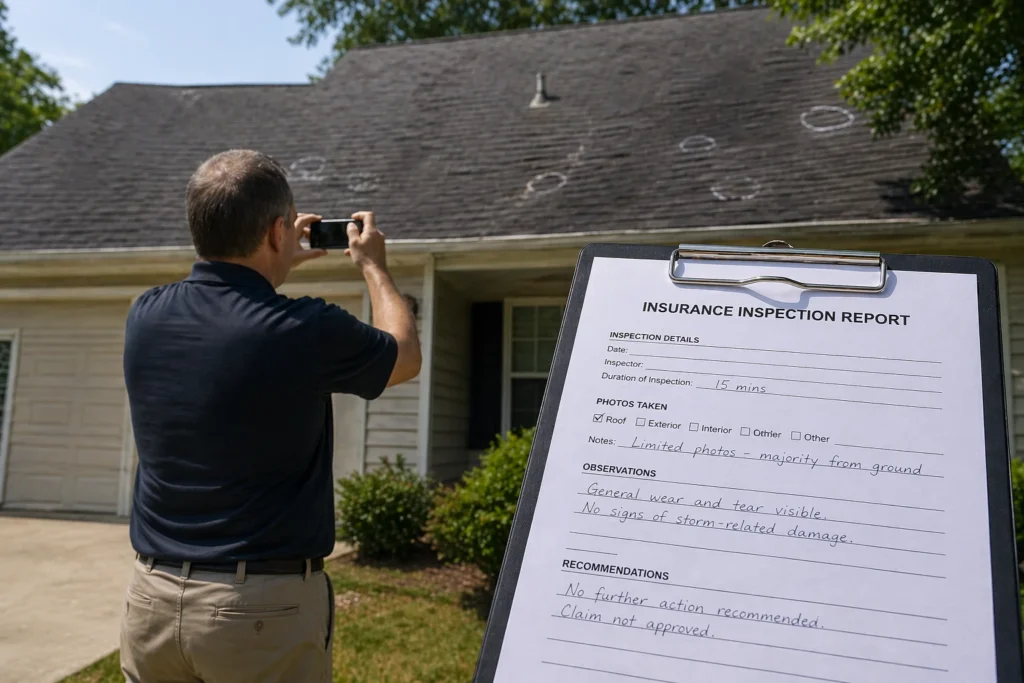

Let’s be real. Not every inspection is thorough.

Common patterns include:

- Short inspections with minimal roof access

- Missing or limited photo documentation

- Reports that understate damage severity

- Technical language that avoids clear conclusions

These tactics create uncertainty. And uncertainty often leads to denial.

What to Do Immediately After a Denial

This is where most homeowners either recover or lose ground.

Step 1: Read the Denial Letter Carefully

Don’t skim it. Break it down.

Look for:

- Specific reasons for denial

- Policy clauses referenced

- Missing explanations

If something feels vague or incomplete, that’s important. It gives you a starting point for your appeal.

Step 2: Request Your Full Claim File

This is non-negotiable.

Ask your insurance company for:

- Adjuster notes

- Inspection photos

- Internal reports

- Damage estimates

This file reveals how your claim was evaluated and where it fell short.

Step 3: Don’t Accept the Decision Yet

This is critical. A denial feels final. It’s not. Many homeowners stop here. The ones who don’t? They often recover significantly more.

Understanding Your Insurance Policy (Without Getting Overwhelmed)

Insurance policies aren’t written to be simple. But you don’t need to understand everything just the right things.

Key Terms That Affect Your Claim

- Actual Cash Value (ACV)

This accounts for depreciation and reduces your payout. - Replacement Cost Value (RCV)

This covers the full cost to replace damaged materials. - Deductibles

Hail deductibles in Texas are often higher than standard ones. - Coverage limits

Your policy caps how much can be paid.

At its core, insurance is built around the concept of indemnity meaning the goal is to restore you to your financial position before the loss, not to profit from it. If you want a deeper explanation of how that principle works, you can review this resource:

Where Insurance Companies Use Complexity

Confusion works in their favor.

- Overlapping policy clauses

- Undefined damage terminology

- Technical wording that lacks clarity

When you simplify the policy, you take control.

Rebuilding Your Claim With Stronger Evidence

If your first claim wasn’t strong enough, your second one must be. This is where denied claims turn into approved ones.

Re-Document the Damage Thoroughly

Don’t assume anything is obvious.

Capture everything:

- Roof shingles (bruising, granule loss, soft spots)

- Flashing and vents

- Gutters and downspouts

- Siding dents or cracks

- Window damage

- Interior ceiling stains or leaks

You’re not just documenting damage. You’re building a case and if you need a deeper breakdown of the process, reviewing a guide on How to Document Hail Damage for an Insurance Claim can help you avoid the exact mistakes that lead to denials.

Upgrade Your Documentation Approach

Better tools = better outcomes.

Use:

- High-resolution photos

- Timestamp-enabled images

- Multiple angles per damage area

- Wide shots for context

Optional but powerful:

- Drone footage

- Moisture detection tools

The clearer your evidence, the harder it is to deny.

Why Independent Inspections Change Everything

This is where the dynamic shifts.

| Inspection Type | Works For | Priority |

| Insurance Adjuster | Insurance company | Cost control |

| Contractor | Mixed | Repair scope |

| Public Adjuster | Homeowner | Claim maximization |

An independent inspection often uncovers missed or misclassified damage.

Filing an Appeal That Gets Results

This is not about emotion. It’s about precision.

Build a Strong Appeal Letter

Your appeal should include:

- Claim number

- Summary of denial

- Specific points you dispute

- Supporting evidence references

Keep it structured. Keep it factual.

Strengthen Your Submission

Add:

- New photo documentation

- Independent inspection reports

- Detailed repair estimates

Each piece of evidence should directly counter the denial.

Timing Matters More Than You Think

In Texas:

- Appeal windows may be limited

- Legal timelines apply

The faster you act, the stronger your position.

Real-World Scenario: Denied vs. Approved Claim

Let’s make this practical.

Scenario A: Weak Claim

- Limited photos

- No independent inspection

- Accepted insurance report

Outcome: Partial payout or full denial

Scenario B: Strengthened Claim

- Detailed photo documentation

- Independent inspection report

- Formal appeal submitted

Outcome: Full roof replacement approved

The difference isn’t luck. It’s preparation.

When to Hire a Public Adjuster in Tyler

Some situations require more than effort. They require expertise.

What a Public Adjuster Does

A public adjuster works exclusively for you.

- Re-evaluates your damage

- Builds a stronger claim

- Negotiates directly with the insurer

When You Should Consider Hiring One

- Your claim was denied

- Damage is extensive

- You’re receiving conflicting information

Why Local Experience Matters

In Tyler, hail claims are frequent. That affects everything.

A local public adjuster understands:

- Storm patterns

- Insurer behavior

- Realistic repair costs

That local knowledge can shift the outcome.

The Appraisal Process: A Strategic Option

This is often overlooked but powerful.

What It Is

- You select an appraiser

- The insurer selects one

- A neutral umpire resolves disagreements

When It Works Best

Use it when:

- Damage is acknowledged

- The dispute is about cost

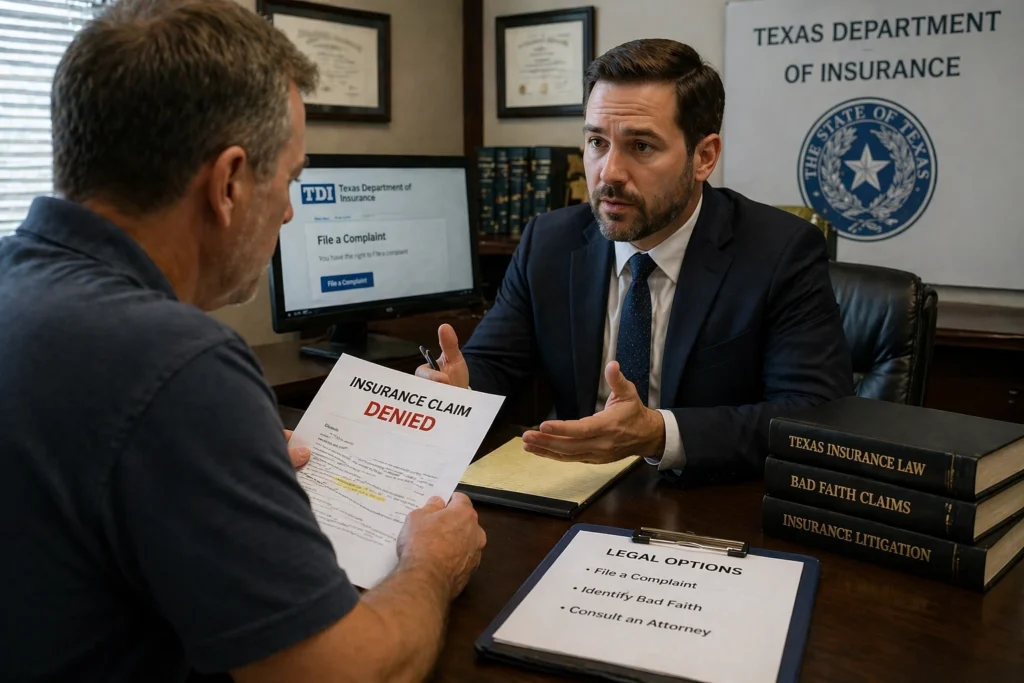

Legal Options If the Denial Stands

If needed, escalate.

- File a complaint with the Texas Department of Insurance

- Identify bad faith behavior

- Consult an attorney for high-value disputes

Turning a Denial Into a Win

If you’re dealing with what to do if your hail claim was denied in Texas, here’s the reality:

- Denials are common

- Many are reversible

- Strong documentation changes outcomes

Stay persistent. Stay strategic. And don’t walk away from money that should rightfully be yours.

FAQs

Yes, you can reopen or dispute a denied claim if you have new evidence or believe the denial was incorrect.

Carefully review your denial letter and request your full claim file to understand why the decision was made.

Deadlines vary by policy, but acting quickly is critical to preserve your rights and options.

You typically can’t file a new claim, but you can appeal or reopen the existing one with stronger documentation.

Yes, an independent inspection can uncover missed damage and strengthen your appeal.

It’s a method where both sides hire appraisers to determine the value of the damage when there’s a disagreement.

You should consider hiring one if your claim was denied, underpaid, or involves significant damage.

Yes, but you can challenge it if you can prove the damage was caused by hail instead.

Not directly, but your overall claim history may influence future rates.

These include unfair claim denials, delays, or misrepresentation of your policy terms by the insurer.